Chief Investment Strategist, The Freeport Society

Boom!

3.3% annualized Q4 GDP growth (after inflation). Economists were only expecting 2%.

Not as good as Q3 GDP numbers, which came in smoking at 4.9%. But still better than a kick in the teeth.

These are good numbers, for sure. And sometimes it’s nice to just take the win.

But because I’m a masochist, let’s dig deeper into the numbers to see if we can find any noteworthy nuggets.

I’ll start with the good news.

While most of the country seems to be in a sour mood, consumer spending tells a different story. It was strong overall in Q4, up 2.8%. But spending on goods (or “stuff”) was up 3.8% with the biggest driver being recreational goods and vehicles.

Spending on services was overall tepid. But spending on food services and accommodations (government-speak for bars, restaurants, and hotels) was strong, helping to pull the average up.

Basically, the American consumer is confident enough about the future to blow a little extra money on family nights out.

It’s worth noting that exports grew at a 6.3% clip too.

Great!

Now let’s take a look at the bad news…

The Dark Underbelly of Spending

The same GDP release reported that federal government spending was up 4.2% for 2023. And let’s be clear, it was already plenty high in 2022. Meanwhile, GDP growth for the full year was only 2.5%.

Hmmm…

Let’s also keep those rosy numbers on bar, restaurant, and hotel sales in perspective.

Yes, it’s great that Americans are dining out and taking vacations. But it seems like they’re doing it with money they don’t have.

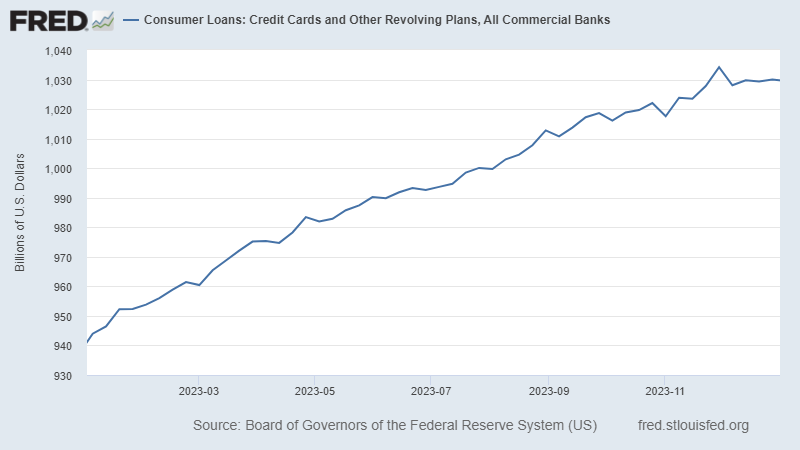

Credit card balances rose nearly 10% last year, ending 2023 at near all-time highs. This is not a chart that should make you or any rational person feel good.

To the extent that Americans do have cash to throw around in restaurants, bars, and hotels, it’s because they aren’t spending it on housing.

Existing home sales finished the year at an annualized rate of 3.78 million homes. That’s more than 40% lower than during the go-go pandemic years. In fact, that puts sales at levels we saw during the 1980s and ‘90s… when there were roughly 100 million fewer Americans than there are today.

So what should you do with all of this data?

What’s the Investment Takeaway?

You know my views on inflation by now. I do not believe that it’s falling fast enough to justify Federal Reserve rate cuts any time soon.

Core inflation, which excludes volatile food and energy prices, is still running at about 3.4%. And inflation in services – which is much harder for the Fed to kill – is still well over 5%.

If the past 20 years have taught us anything it’s that artificially low interest rates inflate bubbles and encourage investment in asinine business models that would never see the light of day in a world where money had real value (ahem, WeWork…).

If Chairman Jerome Powell and his posse were capable of learning – and this is dubious at best – then they would err on the side of keeping interest rates at least slightly higher than they think they should be. It might – might – help us avoid yet another asset bubble.

I don’t expect the Fed will take my advice. Nothing about the experience of the last two decades suggests they’re capable of learning from their mistakes.

Our saving grace is the stronger-than-expected GDP reports. In light of a confident – albeit indebted – American consumer, the Fed will almost certainly postpone its plans to cut rates.

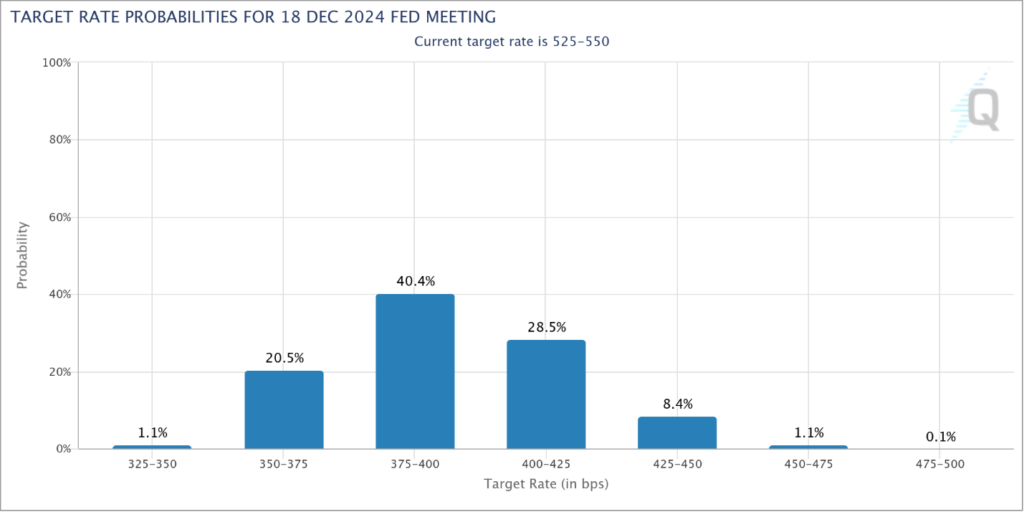

We already see this reflected in the futures markets (see chart below).

The futures market is now pricing in a 62% chance that the Fed cuts rates by at least 1.5%. Last month, it was pricing in an 82% chance of a cut at least that deep.

The Fed will cut rates. They pretty much have to at this point because they’ve been telegraphing that this is the plan for months. Not cutting rates would make them lose face. But the stronger the GDP numbers continue to be, the less the Fed will cut and the slower they will get around to doing it.

This is a long way of saying that the “risk on” market of 2020 and 2021 isn’t coming back in a hurry.

That’s good.

If I had to suffer through another year of obnoxious meme stock stories, I might run away to the wilds of Argentina and never come back. And I say this as I write from Lima, Peru, which is already pretty close to the edge.

But this means that we’ll need to be more selective about how we invest and where we look for growth.

That’s why we are focusing our attention on five core themes – dollar devaluation, exponential progress, deglobalization, rebuilding America, and energy – where the most investment opportunities lie. These are also the five areas that will ride through the presidential election chaos better than any others. Watch this special presentation to discover the details.

To life, liberty, and the pursuit of wealth.