Chief Investment Strategist, The Freeport Society

We can stick a fork in 2023. It’s done.

But what kind of a year will 2024 be?

Will we see that perfect Goldilocks scenario in which inflation continues to fall… yet the economy manages to avoid a recession?

Or will 2024 be the year when the chickens finally come home to roost and the market reprices to reflect a new normal of higher interest rates and more modest growth?

Or might we somehow get a little bit of all of the above?

Let’s dust off our crystal balls and look into the next 12 months.

You don’t have to be blessed (cursed?) with the gift of prophecy to know that 2024 will be a chaotic election year.

I am more certain that next year will be the most chaotic election of our lifetimes than I am that the sun will rise in the east tomorrow.

Four years after the 2020 election – which was, up until today, the most chaotic election of our lifetimes – nothing has changed. Not even the candidates.

Right now, we’re looking at a rematch of Joe Biden and Donald Trump… two candidates well past their respective shelf lives… and that most Americans would prefer to do without, if the polls are anywhere close to accurate.

Here at The Freeport Society, we expect a third candidate to enter the ring come August 19. Our friend, Louis Navellier, shares the details in a special presentation. Watch it ASAP, here.

While I’m making predictions with 100% confidence, let me throw out another…

We won’t see anything resembling fiscal responsibility from Congress or the White House in 2024.

By the government’s own estimates, we’re looking at a $1.8 trillion budget deficit next year. It will borrow close to $2 trillion… but none of it will go to investments in the future. About a trillion of that amount will go to pay interest on debts already racked up, with the rest earmarked for current expenses.

I pity my poor children, who will be left to clean up this mess decades from now.

But let’s return to our crystal balls here.

As Hopeful As a Kind In a Candy Store

One of the ongoing themes we focus on at The Freeport Society is dollar devaluation. This didn’t start with the post-2020 inflation surge. You could argue – and I have, repeatedly – that it started with the creation of the Federal Reserve in 1913… progressively got worse for the remainder of the 20th century… and then collapsed into absolute debauchery after 2008. Since then, it’s plumbed depths I never imagined possible.

Our country’s $33 trillion debt pile was only made possible by a servile Fed willing to accommodate a spendthrift congress and White House via rate manipulation and quantitative easing.

In a brief moment of sobriety, the Fed raised interest rates from effectively zero to a target of 5.25% to 5.50% in an attempt to stamp out inflation.

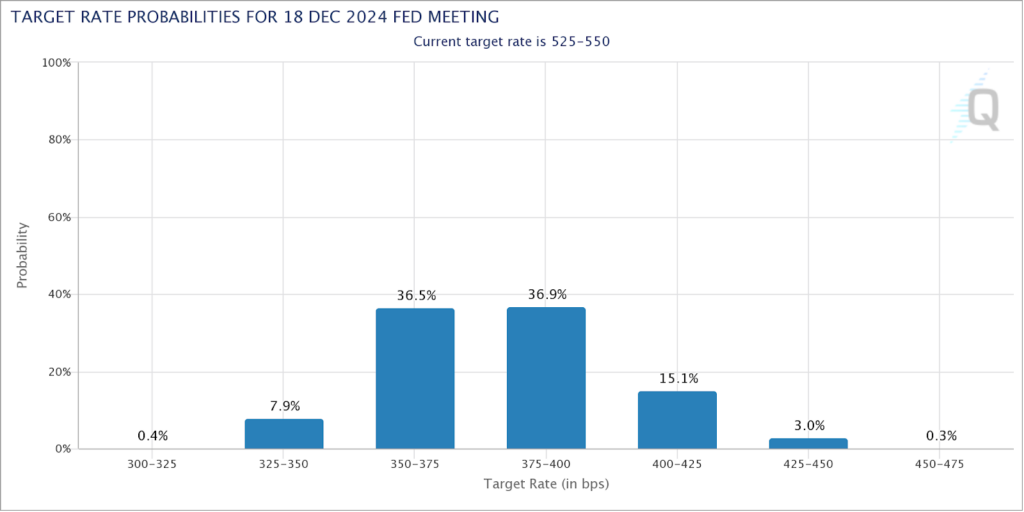

But take a look at what Wall Street is forecasting for 2024…

The Fed Funds futures market is pricing in a better than 80% chance that the Fed will cut rates by at least 1.5%… which would mean the Fed would cut its standard 0.25% in six out of the eight scheduled meetings next year.

The market is also pricing in a better than 44% probability that they cut rates even further. Take a look at this chart, showing what Wall Street anticipates…

Source: Chicago Mercantile Exchange

I have my doubts about that.

Inflation in services is stickier than inflation in goods, and the Fed is effectively fighting demographic trends it can’t control.

While I will never bet against the Fed’s willingness to destroy the dollar’s value with overly stimulative interest rate policies, I think Wall Street is getting ahead of itself here.

The more likely scenario is that the Fed cuts rates just enough to erode the dollar’s credibility… but not enough to launch a major bull market in stocks and other risky assets.

We’ll see.

We already have several strong investment recommendations in The Freeport Investor to protect our portfolios against the Fed’s folly. But until we see monetary sobriety from the Fed – and I’m not holding my breath – I’ll continue looking for more.

Will We Get a Recession In 2024?

The crystal ball is a little more clouded on this one.

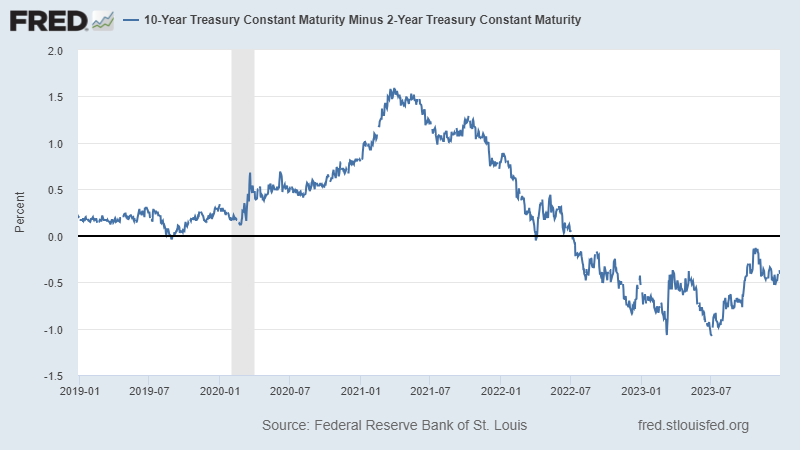

Historically, an inverted yield curve – a situation where short-term rates are higher than long-term rates – has been a nearly foolproof recession indicator. Since 1955, every yield inversion but one – a false positive in 1966 – predated a recession.

And as you can see in the chart below, the 10-year yield has been lower than the two-year yield for nearly two full years.

Could it be that we get another false positive here?

Maybe.

But other indicators point to a recession as well.

The Conference Board’s Index of Leading Economic Indicators has been pointing lower for months. As the Conference Board explains,

The U.S. LEI continued declining in November, with stock prices making virtually the only positive contribution to the index in the month Housing and labor market indicators weakened in November, reflecting warning areas for the economy. The Leading Credit Index™ and manufacturing new orders were essentially unchanged, pointing to a lack of economic growth momentum in the near term. Despite the economy’s ongoing resilience… the U.S. LEI suggests a downshift of economic activity ahead. As a result, The Conference Board forecasts a short and shallow recession in the first half of 2024.

– Justyna Zabinska-La Monica, Senior Manager, Business Cycle Indicators at The Conference Board.

We’ll see if we get that recession… or if the economy manages to muddle through. But either way, my recommendation is that we focus on investment themes with staying power.

This starts with a focus on quality. The strongest American companies have proven their ability to profit through boom or bust, inflation or deflation. I call them the “Rich Man’s Currency,” and they are a critical piece of our portfolio in The Freeport Investor.

I also see major opportunity in the backlash to environmental, social, and governance-based (ESG) investing. Our oil and gas sector has been neglected for the better part of a decade as new capital investments have gone mostly to renewable projects like solar and wind. The result is an energy sector that is cheap, under-owned, and well-positioned to deliver really solid returns in 2024 and beyond.

And that’s not all.

2023 was a year of deglobalization, as the United States and China continued a nasty economic divorce. This has been a contributor to the nasty spike in prices over the past few years, as undoing 40+ years of integration is expensive and messy.

But this massive reshoring is also creating opportunities for us. I call it the rebirth of American manufacturing, and we’re still in the very early innings.

Of course, I can’t tell you exactly how 2024 will unfold. No-one can. But I can tell you I’m wildly bullish on the opportunities I see, and I’d love for us to profit together. Find out how in this special presentation.

To life, liberty, and the pursuit of wealth…