Chief Investment Strategist, The Freeport Society

“Government is best which governs least.”

Henry David Thoreau, who quoted the above in his 1849 Civil Disobedience, is not wrong. We need basic rules. Don’t steal, don’t kill, don’t run a Ponzi scheme… that sort of thing.

But rules must make sense. They shouldn’t be arbitrary or overly burdensome. And importantly, the person making the rules must have the authority to make them.

So I’m flummoxed why the Securities and Exchange Commission is making environmental rules.

The SEC is the securities regulator… they police the stock market.

Its mission statement is “to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation.”

And by “protect investors,” it means safeguarding them from financial fraud or the likes of the next Bernie Madoff.

It’s a stretch to suggest the SEC exists to protect investors from global warming or rising sea levels.

Last time I checked, that was under the purview of the Environmental Protection Agency.

Yet here we are.

So let’s consider what we, as Freeport Society members, can do to invest successfully within the SEC’s newly introduced, and burdensome, impediment to capitalism.

Among the new requirements, all publicly traded companies must now disclose….

- Climate-related risks that have had or can have a material impact on the company’s business strategy, results of operations, or financial condition.

- Information about the company’s climate-related targets or goals, if any, that have materially affected or could likely materially affect its business, results of operations, or financial condition. Disclosures would include material expenditures and material impacts on financial estimates and assumptions that result directly from the target or goal, or actions taken to achieve it.

- For large accelerated filers (LAFs) and accelerated filers (AFs) that are not otherwise exempted, information about material Scope 1 emissions and/or Scope 2 emissions.

Note that I simplified the language in the above to make it more intelligible.

I have so many questions…

Is additional, carefully crafted legal language in a company’s annual report to explain the business risk posed by Florida hurricanes going to improve anyone’s investment decisions?

Besides, what the hell determines what’s “material”?

But it’s that last bullet that really gets me.

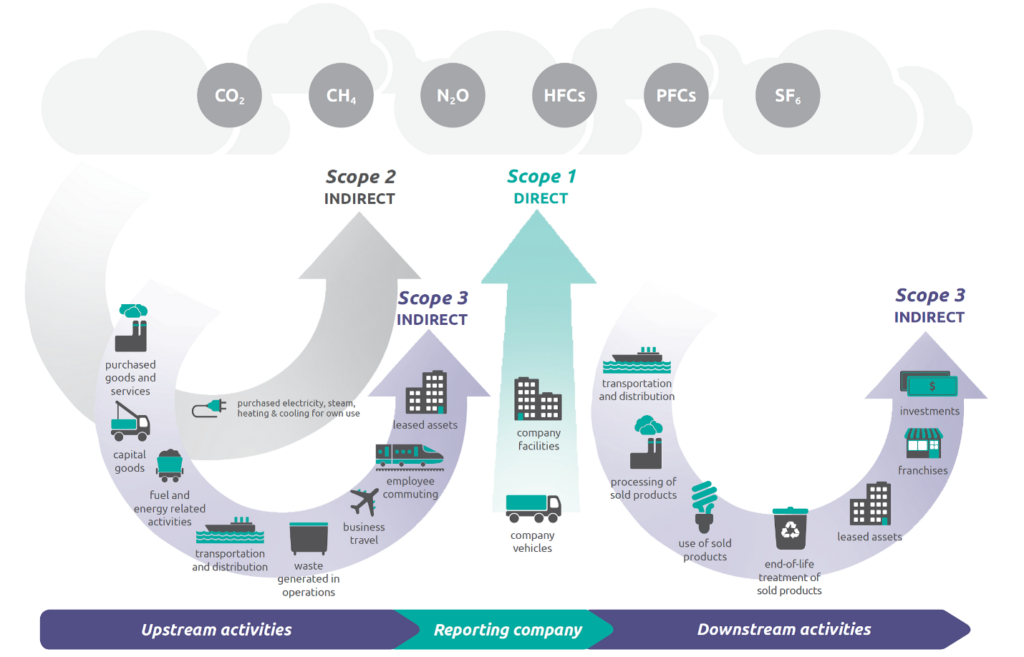

In plain English, companies (“fliers”) must estimate (read “guess”) and report their carbon emissions. Depending on the criteria they meet, the level of that reporting varies. The graphic below helps explain this…

Emissions Reporting Requirements

Per the EPA…

Scope 1 emissions are direct greenhouse emissions that occur from sources that are controlled or owned by an organization (e.g., emissions associated with fuel combustion in boilers, furnaces, vehicles).

Scope 2 emissions are indirect GHG emissions associated with the purchase of electricity, steam, heat, or cooling.

Basically, Scope 1 means the company is responsible for reporting their personal emissions.

Scope 2 means it’s responsible for also reporting the emissions of all contractors and partners along its supply chain.

There’s good news.

Scope 3 reporting was dropped at the last minute. That would have required every company in America to report on emissions from their customers as well.

Hmm.

Frankly, I wouldn’t have the foggiest idea how to quantify the amount of greenhouse gas burned by each of my readers when they took a few minutes out of their day to read this on their phone or computer.

Fear not. A handsomely paid environmental consultant with friends in government knows how to do that for me!

Those people don’t come cheap. According to the Competitive Enterprise Institute,

Under the SEC’s own calculations, the average firm will pay an extra $864,000 for the mandated disclosures, though some analysts believe the actual cost will be higher. Firms will also be forced to hire lawyers, accountants, and [Environmental, Social and Governance] ESG experts to contend with the rule’s estimated 39 million additional hours of paperwork. [emphasis mine]

Look, I’m not an anarchist, my general disdain for authority notwithstanding. Like I said, we need securities rules to protect investors from financial crimes. We need environmental rules to protect the air we breathe and the water we drink.

We don’t need the securities regulator creating a make-work program for the ESG consulting industry… and 39 million hours of additional paperwork on top of the untold hundreds of millions of hours already lost to red tape.

All that does is discourage companies from going public, which would reduce the stocks available to investors like you and me.

This contradicts the SEC’s own “facilitate capital formation” mandate.

When Warren Buffett said that ESG reporting was “asinine,” this is what he was talking about.

The Oracle of Omaha knows that emissions estimates made by ESG consultants in Excel spreadsheets add no value – either to the environment, a company’s bottom line, or investor returns.

Yet they sure do create a lot of expensive paperwork!

This is yet another major burden on smaller public companies and an impediment to those that are thinking about going public.

The best solution for us investors, under these circumstances, is to find companies big enough, strong enough, and connected enough to navigate any bureaucratic mess the feds care to throw at them.

Stick with the best, the companies that I call the “Rich Man’s Super Currency.”

We already have several of these in our Freeport Investor model portfolio. Myself and Freeport Society friend Louis Navellier explain what these are and the many other reasons for why they’re so important to your investment strategy in this video.

To life, liberty, and the pursuit of wealth.