Chief Investment Strategist, The Freeport Society

“The WORST…”

“A real dummy…”

“A numbskull…”

“An obvious Trump hater…”

There’s clearly no love lost between President Trump and Fed chair Jerome Powell.

Lately, Trump has been unloading on the central banker on social media.

He even managed to clear some time at a NATO press conference this week to remind the world that he believed Powell to be an “average-minded person” with a “low IQ.”

Trump doesn’t have the authority to fire Powell.

Under the Federal Reserve Act, a president cannot remove a Fed governor or chair just because they disagree with their policies.

So, Mr. Transitory Inflation will still be running the Fed for another 11 months, until his term ends.

But Trump announced this week that he had already narrowed down Powell’s replacement to a handful of candidates… and that an announcement might be coming soon.

As investors, we need to pay attention.

The Federal Reserve Chair is one of the most powerful positions on the planet. In terms of economic clout, it’s more powerful than the presidency. The candidate that Trump picks matters.

So, today, let’s look at…

- The significance of an early announcement to replace Powell

- Who Trump is considering for the job

- What this means for our investments

As you’ll see, no matter who gets the top job, we’ll continue to recommend you hold “anti-dollars” as part of your long-term portfolio.

A Short List of Doves

First, to state the obvious, Trump is wildly unpredictable.

His decision may come after long, careful deliberation with his closest advisors. Or he may pick a CNBC host on a whim because he thought they looked good on camera, and they happened to be on the air saying something he liked at the moment he made his decision.

We’ll know when we know.

In the absence of hard data to work with, let’s look at what the betting markets are saying.

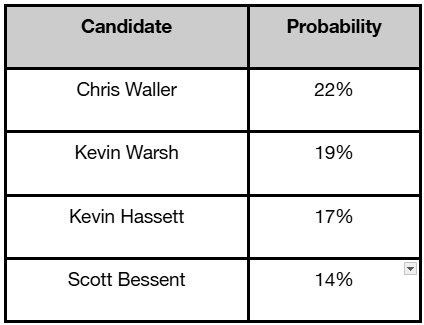

The betting site Polymarket has open contracts on the candidates, summarized in the table below.

At the top of the list is Chris Waller.

In 2020, Trump nominated him to serve as a member of the Federal Reserve Board of Governors. Betting markets are giving him a 22% chance of getting the nod – making him the most likely replacement.

Waller is considered to be the most dovish member of the board, meaning he’s the most open to cutting interest rates sooner rather than later.

He’s on the record saying that he believes any inflation coming from Trump’s tariffs will be one-off in nature, which is presumably why he makes the top of the list.

That would be good news for the stock market, as long as inflation doesn’t come roaring back again as a result.

Next in line, with a 19% probability, is Kevin Warsh – a former Fed governor from the Bush and Obama years with strong ties to Wall Street.

Warsh is an odd choice because during his time at the Fed he was known as a hard-money hawk with no tolerance for inflation. But more recently, he’s expressed a willingness to cut rates, which was apparently enough to get him on the short list.

Kevin Hassett is up next, with a 17% chance of winning, according to betting markets.

He’s never served as a Fed governor, although he did work as an economist for the Fed. And he’s one of the architects of Trump’s economic policies in the White House.

Trump tends to prize loyalty. He likely assumes that Hassett would be an ally at the Fed.

Rounding out the top four is Treasury Secretary Scott Bessent, with a 14% chance based on current betting odds.

From what I can tell, Bessent has been quietly running the government for the past few months – even taking on roles that wouldn’t normally be associated with a Treasury Secretary.

It was Bessent, rather than the more obvious Commerce Secretary Howard Lutnick, who Trump sent to London to negotiate a trade deal with China.

Bessent has no direct experience with central banking. But he has strong ties to Wall Street… he’s generally viewed as competent… and Trump trusts him.

The biggest problem with Bessent taking the job is that he would leave a gaping hole at the Treasury at a time when the U.S. is due to roll over $11 trillion in maturing bonds.

In what will likely go down in history as the single worst financial decision of the republic, Janet Yellen and Steve Mnuchin missed the opportunity to refinance substantially the entire federal debt for 30 years when the yield was scraping along at less than 1.5%.

Now, over the next 12 months, we have $11 trillion of the $36 trillion maturing… and needing to be rolled over at what is now a vastly higher rate.

If handled poorly, that’s the sort of thing that could tank the bond market.

It’s Different This Time

It’s not unusual for a president to announce his pick for Fed Chair a few months early.

That allows the incoming chair to coordinate with the outgoing chair and ensure policy continuity.

The last thing Mr. Market wants to see is instability at the head of the world’s most powerful central bank.

Powell, Yellen, and Ben Bernanke were all announced three to four months before their predecessor’s retirement.

But it’s different this time…

If Trump names his choice soon, it won’t be to ensure continuity. It will be to announce a public change in policy direction with the specific goal of neutering Powell.

Powell might still nominally be in charge. But Mr. Market will be listening to his replacement’s comments for clues as to what policy moves might be coming down the pike.

Does that really matter?

Will it have a real impact on the market?

It’s easy to forget that Trump appointed Powell at the beginning of his first term. And there’s no guarantee that a new appointee will automatically do his bidding or respond to every tweet or Truth Social post.

And while the four candidates on the short list may be more inclined than Powell to cut rates, I don’t see any of them as being willing to take orders from the White House.

Every indication is that they’d take the job and its independence seriously.

Of course, that doesn’t mean they’ll actually be good at the job…

The Fed’s Fake Money Problem

Powell gave us “transitory” inflation that still lingers five years later…

Yellen and Bernanke gave us “helicopter money” and “QE to infinity”…

And Alan Greenspan’s famous “put” – his inclination to drop rates whenever the stock market was in trouble – helped fuel the 1990s dot-com and the 2000s housing bubble.

It was a group effort by these clowns to get us where we are today, fighting “transitory” inflation and the aftermath of a quarter century of financial bubbles.

And I don’t see any of Trump’s picks being better or worse than their predecessors.

The end result will still be more fake money to finance more deficit spending and racking up more debt… leaving our children and grandchildren a real mess to clean up

The problem isn’t Powell’s hesitancy to lower rates – the problem is a corrupted and manipulated currency.

If interest rates were truly set by the market, do you think they would have been as low as they were for the past 25 years?

And if Uncle Sam didn’t have a captive buyer for his debt from a compliant Federal Reserve – and actually had to appease real-world investors allocating their hard-earned capital – do you think Congress would have been able to spend us $36 trillion into debt…

Or bail out criminally inept banks…

Or build out a socialist welfare state…

Or engage in a series of mind-numbingly stupid and expensive foreign wars?

Without the avalanche of cheap money from the Fed, would we have had the dot-com bubble?

The housing bubble?

The alphabet soup of mortgage derivatives that blew up the world (CMO, CDO, MBS…)?

The FOMO (fear of missing out) market?

BTFD (buy the f’ing dip)?

Or, my personal favorite, the bubble in bored ape NFTs?

I’ll answer for you.

No.

This is why Bitcoin was created in 2008. It was a rational reaction to the explosion of government debt made possible by a servile central banking system.

It’s also why gold has been valued as a store of value for millennia.

We’ve held both in the Freeport Investor model portfolio since its launch in December 2023. We’re up 157% and 64%, respectively.

As long as our dollar is being managed by a fundamentally flawed Federal Reserve system, I don’t intend to sell either.

To life, liberty, and the pursuit of wealth.