Chief Investment Strategist, The Freeport Society

Fortune rarely favors the pessimist.

To the risk takers go the spoils.

And it’s usually a terrible idea to bet against the market.

Growing companies in a growing economy almost always translate into rising stock prices, at least over the long-term.

But…

That playbook doesn’t work for every market.

Take U.S. growth stocks – stocks priced higher than average relative to earnings because investors are paying today for tomorrow’s growth.

They tend to outperform over time.

But they also go through long periods of underperformance relative to value, income, or international stocks.

So, the Magnificent Seven – Apple, Microsoft, Google, Amazon, Meta, Tesla, and Nvidia – that have dominated the market for years are not preordained to lead the market higher forever.

In fact, these popular stocks may underperform the broad market over the next decade.

And if the history of the last quarter century is any guide, now is a good time to lighten up on tech and buy into some long-neglected pockets of the market instead.

I’m going to help you do just that today.

Time for a Growth Stocks Breather

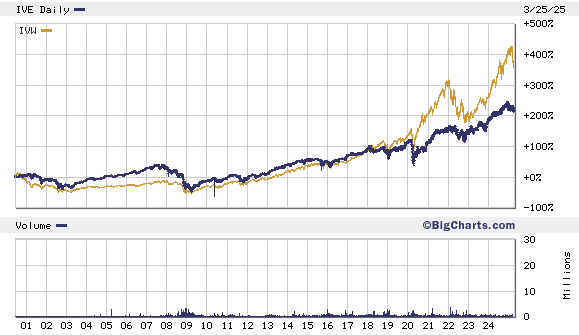

It’s all in the chart below…

It compares the performance of growth stocks relative to value stocks. These are stocks that appear to be undervalued by the market relative to their fundamentals.

And it does that using the iShares S&P 500 Growth ETF (IVW) and iShares S&P 500 Value ETF (IVE) as proxies.

The IVW is the orange line and the IVE is the dark blue line.

As you can see, over the past 25 years, growth stocks have outperformed value stocks by about 150%.

But all of that outperformance has come in just the last six years… a time that included the pandemic, unprecedented Fed and Congressional stimulus, and investors’ FOMO (fear of missing out) attitude to risk.

By contrast, between 2000 and 2019, value stocks performed as well or better than growth stocks. And immediately following the tech bubble, they beat the pants off of growth stocks.

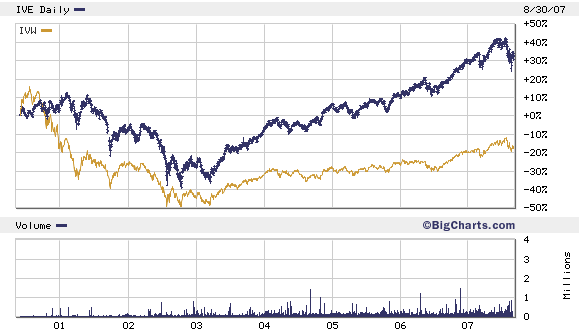

Let’s zoom in on the 2000 to 2007 window.

In the seven years between the dot-com bubble and the housing market collapse in 2007, value stocks destroyed growth stocks. They outperformed by more than 50%.

More important, they ended that period in positive territory. By the time the market rolled over in late 2007, growth stocks were still more than 10% below their 2000 levels.

And we could be about to enter another period in which value outperforms growth.

This Market Is Ripe for New Leadership

Think about how stocks are valued.

Stocks are priced today based on what investors expect them to earn in the future relative to what they can earn on bonds.

Usually, Wall Street does a decent job of pricing stocks.

But sometimes, particularly after a long stretch of outperformance, the expectations get unrealistic.

Eventually the company fails to deliver on those ridiculously high expectations, and then the stock price drops to reflect the newer, more modest outlook.

The same happens with stocks that are out of favor.

Wall Street expects little out of beaten down value stocks. Eventually, they get cheap enough to beat the low expectations built into their prices.

Also, when a trade works, it eventually gets crowded.

Momentum begets momentum, success begets success, new investors keep piling in… until there’s simply no one left to buy.

On the flip side, once a stock is so out of favor that virtually everyone has dumped it, there’s no one left to sell… and it finds a bottom.

No one rings a bell at the top (or the bottom, for that matter).

I can’t tell you for sure that the Magnificent Seven’s monster run is over.

But I can tell you that the trade got crowded a long time ago…

The shares are expensive by any rational metric – price/earnings, price/sales, dividend yield, CAPE… Pick any or all of them and they will tell you the same story.

The market is ripe for new leadership.

Value stocks outperformed after the last major tech boom in the 1990s and early 2000s.

I think we’ll see a similar outperformance this time around.

How a Single Investment Can Change Your Life

That said, over a long investing career, you should include quality growth stocks.

If you find just one Nvidia or Tesla early and hold on to it, the profits you make can change your life.

I know this from personal experience.

If you’ve read my work for any length of time, you know that my grandfather was my mentor.

His work ethic was an inspiration. I watched him work two jobs well into his 70s. But he also found time for family.

His enthusiasm for investing is the reason I got into this line of work.

My pitiful attempts to play the saxophone are also a tribute to him. He was a jazz man until the end.

Yes, he was a good stock picker. But it was one single investment that changed the trajectory of his life.

He bought Walmart when it was still a fledgling upstart retailer from rural Arkansas… and he held onto it for the rest of his life. His profits from that one investment paid for my grandmother’s retirement and for my college tuition and my sister’s college tuition.

So, this isn’t an “either/or” thing.

Don’t abandon growth altogether. You’re probably not going to find that one life-changing investment digging around in the value stock bin.

But also carve out room for quality blue chips in steadier sectors outside of tech. Because they can keep you afloat during those long stretches when growth stocks as a whole just aren’t working out.

Introducing the Rich Man’s Super Currency

It’s what we do with our Rich Man’s Super Currency recommendations at our flagship Freeport Investor advisory.

If you haven’t heard the term before, don’t worry.

It’s our way of describing stocks in elite businesses that generate consistent cash flows.

We call these stocks the Rich Man’s Super Currency because these businesses compound profits over decades and pay out reliable, extremely safe income to their shareholders.

That’s why so many of the world’s high-net-worth individuals own them.

There’s no set definition of an elite business. But they share a handful of common traits…

1. A Durable Competitive Advantage

Walmart has a durable competitive advantage because its huge global distribution network allows it to sell goods at unbeatable low prices.

It’s extremely difficult for smaller firms to compete against that.

2: An Outstanding Brand Name

Coca-Cola is a good example. Its logo is recognized across the world, and people associate it with quality soda. It looks and feels like America.

That’s a competitive advantage virtually impossible for any would-be competitor to overcome.

3. The Largest Business in Its Industry

When you run your business better than the competition, you can’t help but become the biggest.

McDonald’s didn’t become America’s biggest fast-food chain because it made the best hamburgers. Let’s face it, the burgers are mediocre at best. It did it by running a better business than its competitors.

4. Sells Everyday Products

An elite business sells products we use almost every day. Think food, oil, soda, medicine, coffee, energy drinks, smartphones, beer, mouthwash, razor blades, and deodorant. These things don’t go out of style.

5. Sells Habit-Forming, Addictive Products

Look at the list of the 20 best-performing U.S. stocks from 1957 through 2003. You’ll see that many of them sold habit-forming products.

Phillip Morris is at the top of the list. This cigarette company was the top-performing S&P 500 stock from 1957 to 2003.

Fortune Brands, once called American Brands, is also on the list. It sold cigarettes and alcohol.

PepsiCo and The Hershey Co. are on the list, too. They sell sugar and chocolate and caffeine – all addictive!

Many drug companies are on the list as well. They include Abbott Labs, Bristol-Myers Squibb, Merck, and Pfizer. People get accustomed – even addicted – to taking medicinal drugs.

And we’re doing well with the Rich Man’s Super Currency stocks we hold in the model portfolio.

Of the seven we have, all but one are in positive territory. And four are showing double-digit open gains – including 65%, 49%, and 34%.

I can’t share the names of the Rich Man’s Super Currency stocks I’ve recommended at Freeport Investor here out of respect to my paying subscribers. But you can get some of the benefit of this approach through the Vanguard Dividend Appreciation ETF (VIG).

It’s a collection of quality American businesses with a history of consistently raising their dividends. To make the cut, a company has to have a string of at least 10 consecutive years of raising their payout.

Accounting figures can be manipulated. But you can’t fudge cold, hard cash. And VIG is chock full of quality companies with a long history of delivering the goods.

To life, liberty, and the pursuit of wealth,

Charles Sizemore

Chief Investment Strategist, The Freeport Society