Chief Investment Strategist, The Freeport Society

During its unusual post-election meeting, the Fed cut interest rates by a quarter point.

That brings short-term rates down to the 4.5%-4.75% range.

But that’s not really the story here.

What grabbed my attention was Fed chair Jerome Powell’s attempt to defend his job…

Reporter: “If [Trump] asked you to leave, would you go?”

Powell: “No.”

Reporter: “Can you follow up on that? Do you think that legally you are not required to leave?”

Powell: “No.”

A man of few words, it seems.

Now, far be it from me to defend Jerome Powell. If we are to assign blame for the explosion of inflation after the pandemic, it’s a three-way race between Powell, Biden, and Trump.

But that he was even asked if he’d be fired shows us what to expect over the next few years.

Inflation will come back with a vengeance.

There’s a lot to unpack here. You may want to sit down and get comfortable.

Bond Prices Are Diving

Now that the election is over, investors are handicapping what Trump’s victory means for stocks and bonds.

Stocks have just had one of their biggest bounces in years in the anticipation that Trump’s tax cuts and more relaxed attitude to regulation will juice earnings.

They probably will. They did last time.

But the bond market is telling a different story.

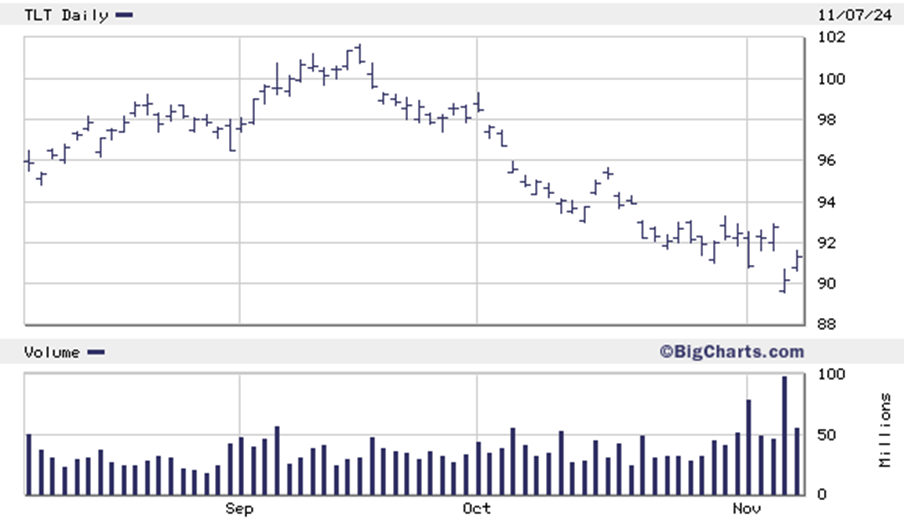

Trump started pulling ahead of Harris in the polls in late summer. That’s when things started going south for bonds.

The iShares 20+ Year Treasury Bond ETF (TLT) tracks prices for Treasury bonds with maturities of 20 years and up.

All bonds are sensitive to inflation. Their prices generally fall when inflation rises because it erodes the purchasing power of a bond’s future cash flows.

Long-term bonds are extremely sensitive to inflation. That’s because they’re exposed to its impact for longer.

In late summer, TLT started sliding. It’s now down a good 10%… with no sign of slowing down.

What does this all mean?

It means the bond market is pricing in the likelihood of higher inflation down the road.

This comes back to election promises… and to the market megatrends we track here at The Freeport Society.

Higher Tariffs = Higher Prices

Let’s start with deglobalization…

The trend since World War II has been to lower trade barriers and reduce tariffs.

But in the early 2000s, that model started to break down as China began flexing its economic muscle in a way that ruffled Uncle Sam’s feathers.

It’s been in full reverse for nearly a decade now.

Trump has pitched a lot of possible tariffs – ranging from 10% to 200%. And it’s not clear whether he intends them to be firm policies or a negotiating tool.

But it’s safe to assume that tariffs will be going higher when he returns to the White House next year.

The president has a lot of freedom to unilaterally set tariff rates. And Trump used that power liberally in his first term.

Biden arguably then out trumped Trump with even higher tariffs on China.

Now, Trump is set to push them higher.

A few tariffs in certain pockets of the economy isn’t going to move the needle much. But a 10% hike in tariff across the board will make all imported goods 10% more expensive.

“Great!” you might say. “We’ll buy American, then. Doesn’t that fix the problem?”

No.

It does not.

Without foreign competition, American producers will charge more. Why wouldn’t they? If given the opportunity to juice a higher profit, I know I would.

Those higher prices are going to show up on store shelves.

The inflation the Fed has tried so hard to stuff back in the bottle is about to bubble out again.

Immigration plays a role here, too.

Lower Rates, Higher Deficits

Biden’s inability to deal with the border crisis is a major reason the Democrats got crushed.

That was an inexcusable mess.

But in fixing the problem, be careful what you wish for.

If you think the labor market is tight now, what’s it going to look like when Trump deports 10 million to 15 million immigrants who’ve been providing cheap labor in the economy?

And how much is it going to cost to find a tradesman to put a new roof on your house or fix a toilet?

It’s safe to assume you’ll be paying higher prices for those services, too.

This brings us back to the Fed.

For all the man’s faults as a central banker – and they are legion – Powell takes the Fed’s political neutrality seriously.

But if Trump acts on his promise to appoint a political loyalist as Powell’s replacement, we can expect lower rates for longer.

During his last presidency, Trump often advocated for lower rates and lashed out at the Fed when it raised them.

The thing is, lower rates fuel not only higher stock prices, but also inflation.

And then, of course, there’s the prospect of a rising budget deficit.

Trump has promised to expand his tax cuts.

Now, you will never hear me complain about lower taxes. But lower taxes without lower spending means higher deficits.

That’s spending money we don’t have.

Spending borrowed money pulls future consumption into the present.

And that’s… you guessed it… inflationary!

So, what do we do about it?

Stocks, Not Bonds, Are Your Best Friend Now

Be wary of bonds.

As I mentioned earlier, bond prices go down as inflation goes up. So, they’re lousy investments in a period of rising inflation.

To the extent you own them at all, stick to short-term bonds. These are less sensitive to the inflation menace.

Instead, it absolutely makes sense to hold onto stocks.

Lower rates, higher deficits, and lower taxes will juice earnings, and that’s a recipe for higher stock prices.

Owning shares in quality, high-margin businesses is your best option for maintaining and growing your wealth in an inflationary environment.

Good, high-margin businesses have pricing power.

They can pass on higher costs to their customers, keeping their margins intact.

These are exactly the types of businesses you want to own… and exactly the ones I look for in The Freeport Investor.

Finally, don’t forget to have dollar hedges in your portfolio. Gold and Bitcoin are core holdings at our Freeport Investor advisory… and likely will be forever. They should be core holdings in your portfolio as well.

To life, liberty and the pursuit of wealth.