Chief Investment Strategist, The Freeport Society

The latest consumer price inflation (CPI) numbers came out yesterday… and given that the results will go a long way to determining whether the Federal Reserve cuts rates following their meeting next month, the financial press took note.

Only… one of these headlines is not like the others. See if you can spot it…

“The Inflation War Has Been Won…”

Forbes

“U.S. Annual Consumer Price Increase Slows to Below 3% as Inflation Ebbs”

Reuters

“Inflation Falls Below 3% for First Time Since March 2021”

Yahoo! Finance

“‘I’m down to eating ramen’: Social Security benefits aren’t keeping up with inflation”

CNN

This wasn’t exactly a hard quiz.

So… what’s the story?

Is inflation really falling?

And if so, why doesn’t it feel like it is?

Five words have the answer…

Lies, Damned Lies, and Statistics

We’ll start with some basic facts.

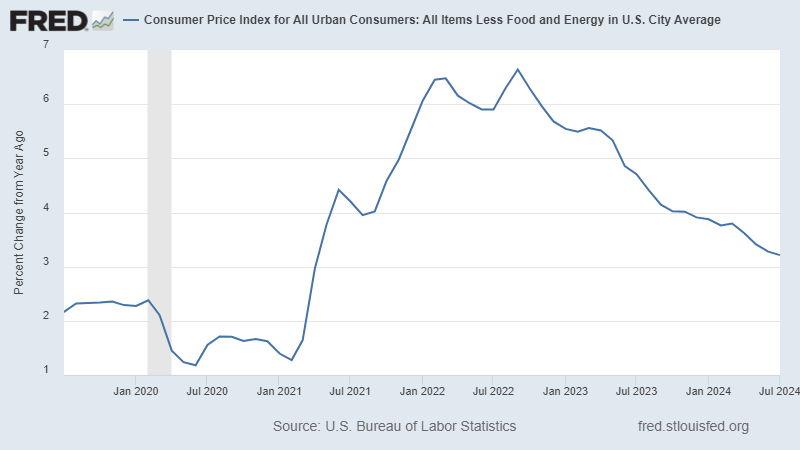

The headline inflation number did indeed drop below 3% for the first time since 2021, finishing the month at a 2.9% clip.

Core inflation, which strips out food and energy, came in a little higher at 3.2%. But that’s still the lowest number we’ve seen in a long time.

Great!

We’ll take what we can get. And I’ll never complain about falling inflation.

But let’s also put those numbers into perspective…

A core inflation rate of 3.2% is a lot better than the 6.5% we suffered through in early 2022. But that doesn’t mean it’s ideal or even tolerable. And it’s still a full 50% higher than the Fed’s target of 2%.

There’s a lot more to unpack here.

To start, what we’re experiencing is disinflation, which means a slowing of inflation. That’s not the same thing as deflation, or falling prices.

Prices are still going up, albeit more slowly than a year ago.

Unfortunately, prices rarely ever go back to where they were a few years ago… or even a few weeks ago. Price hikes are almost always permanent.

But there’s more going on here.

The CPI is an average. It’s designed to give us a quick and dirty idea of how quickly average prices are rising. That doesn’t mean that all prices are rising at exactly 3.2%. There are plenty of pockets of the economy where prices are running at a much faster clip.

Take services, for example.

The costs of services not related to energy, everything from dog grooming to brain surgery, rose at a 4.9% rate in July. In fact, services inflation has been running consistently hotter than goods inflation all year, and there’s a reason for that. Services are people-intensive, and we’re still in the midst of a labor shortage driven by the retirement of the Baby Boomers.

That’s not something the Federal Reserve can kill with a few rate hikes. As I discuss in a recent video presentation, the only way to really fix a demographic-based labor shortage is with productivity-boosting technology.

That’s coming, of course. That’s what all the AI hype is about.

Investors and the mainstream media may be throwing a party because CPI came in cooler… but the rest of us are tightening our belts, shopping more at Walmart (WMT), and eating more Ramen noodles.

There are the statistics and there’s reality. Separating them is a wide canyon. When ordinary citizens hear the cheers, they get angry… and even distrustful of a media reporting stories that are wildly disconnected from their everyday experiences.

What do you do about it?

You invest smartly.

Invest in cash cow companies that pay dividends.

Invest in businesses that are chaos-proof… those like Walmart, as an example.

And absolutely have dollar hedges in your portfolio.

As we barrel toward the November 5 presidential election, this will become even more critical.

Here’s why…

The Going Gets Harder From Here

Dollar strength has kept inflation somewhat in check.

Money tends to flow where it’s treated best – to countries with the highest real interest rates.

After the Federal Reserve raised interest rates to 5.5%, money started flowing out of Japan and other lower-rate countries into U.S. dollars, helping to push the greenback to multi-decade highs.

But the Fed is planning to start cutting rates. So this situation is likely to reverse. This unwinding of the Japanese yen “carry trade” is what roiled the markets last week and may be a taste of things to come.

Why does that matter?

Because, for all of President Joe Biden’s and Donald Trump’s efforts to reduce our dependence on China and other “frenemy” trading partners, the U.S. still imports a lot more than it exports. Last year, the trade deficit was close to $800 billion.

A strong dollar makes imports cheaper… which helps to keep a lid on inflation.

A weaker dollar does the opposite… so, as this unfolds, we’ll have a new inflationary headwind to look forward to.

Sure, inflation is falling. Prices aren’t going up as fast as they were in recent years. We should be happy about that.

But we should also be realistic. The going gets harder from here, and each additional 0.1% decline gets tougher than the one before it due to these demographic and monetary headwinds.

I go into more detail in this video presentation, but here’s what it boils down to:

Build a financial moat around yourself to buffer the insidious and ongoing effects of inflation. It’s one of the best ways to ensure you don’t need to resort to eating only Ramen noodles every day.

To life, liberty, and the pursuit of wealth.