Chief Investment Strategist, The Freeport Society

“Full faith and credit.”

That’s what backs the dollar, U.S. Treasury securities, and essentially the entire banking system: The full faith and credit of the United States government.

Great!

But what does that actually mean?

Not much. It simply means that the government pays its debts… in its own freshly printed dollars.

If that fails to give you a sense of confidence… well… you’re not alone.

My Freeport friend John Pangere has a good take on this. John was once an investment banker… he’s successfully traded currencies, futures, options… and he’s profitably invested in stocks and real estate for years. He’s also the brains and passion behind Rogue Strategic Trader.

Over to you, John…

To life, liberty, and the pursuit of wealth,

Charles Sizemore

Chief Investment Strategist, The Freeport Society

Money for Nothing and the Tips for Free

By John Pangere, Senior Analyst, Rogue Strategic Trader

The Three Stooges were way ahead of their time.

I don’t mean in the sense of their comedy. Although that’s also true.

I mean that 67 years ago they had a far better sense of how our banking system works than most people… even today.

At the beginning of the 1957 episode “A Merry Mix-Up,” Moe wants the $20 that Larry owes him.

Larry only has $10, so Moe takes it. Larry still owes him another $10. But Moe owes Joe Besser – the forgotten sixth stooge – $20. So Moe gives him the $10 he just got from Larry.

It turns out Joe also owes Larry $20. So the original $10 goes back to Larry.

Larry gives that $10 back to Moe to pay off the full $20. And back again to Joe. Then one more time to Larry, who says, “Good! Now we’re all even.”

What happened?!

Nothing.

The money circled around and around until it ended up in the same place it started. (You can watch a clip of that scene here.)

It was comedic genius. And in just 20 seconds the Stooges explained how the banking system works.

More important than understanding how banking works is realizing how fragile it is.

And that it can explode at any minute… unless you know how to avoid the traps.

Spending Never Stops

We’ve all heard the saying, “There are only two certainties in life: death and taxes.” We can add government spending to that, as my Freeport Society friend Charles Sizemore has said before.

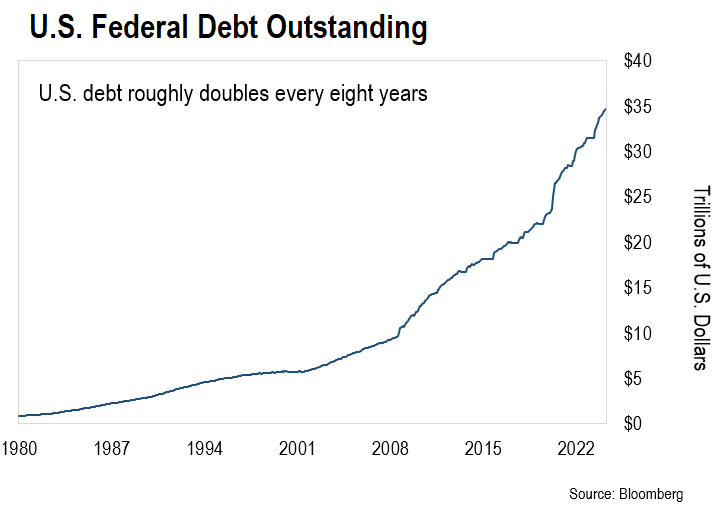

The best way to view that is by taking a look at government debt.

The U.S. government debt load just about doubles under each two-term president (so every eight years.)

Under Ronald Reagan, the debt grew 185%.

Under George W. Bush, it grew 93%.

Under Barack Obama, it grew 78%.

George H.W. Bush and Bill Clinton together sent it up 111% over a combined 12 years.

With Donald Trump, the debt spiked $7.2 trillion in four years. That’s a 36% increase.

And so far, with President Joe Biden, nothing is much different. The debt is up over 25%. Combined with Trump, it’s up 74% in seven years. Which is to say it won’t take much more to hit that doubling point.

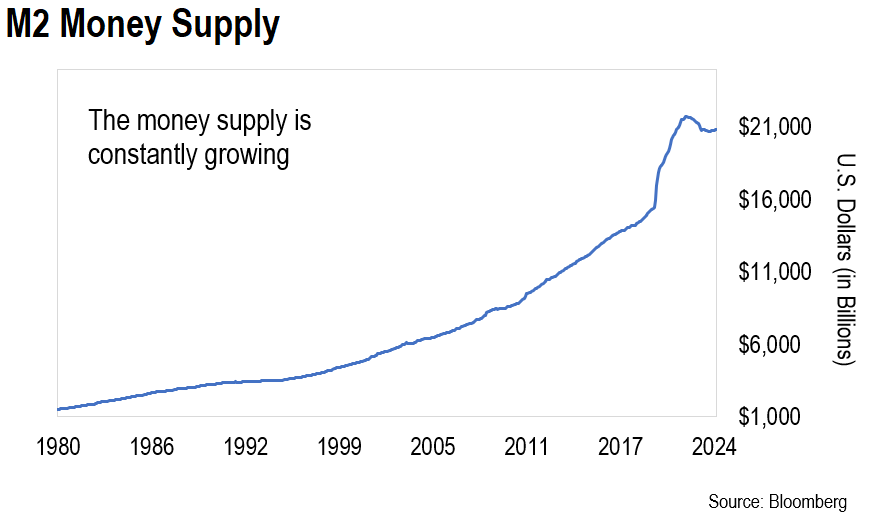

All of this is only possible with a complicit banking system and a Federal Reserve willing to play ball.

The Fed has direct influence over the money supply. That’s the money circulating inside the banking system.

And just like with government debt, it’s a near constant increase over time. Take a look…

The consequences go beyond having more debt. It also leads to inflation, which is something Charles Sizemore talks about regularly in his essays. Said another way, it reduces the value of the dollars in your pocket. After all, every dollar created must go somewhere… even if the trick is moving it round-and-round like The Three Stooges.

Money for Nothing and the Tips for Free

Our system of fractional reserve banking means that a bank doesn’t have to keep all of the money you ask it to secure. It will typically lend most of that money out to others and keep the resulting interest as profit.

When things are steady, the system works well. But when things go haywire, the system can collapse in a hurry.

You can see this by a quick look at pretty much every negative economic event since the turn of the 20th century. A breakdown in the banking system played a significant role in each instance.

The Knickerbocker Crisis of 1907. The Great Depression. The savings and loan crisis of the 1980s. The 1997 Asian banking crisis. The Great Financial Crisis of 2008.

Each one of these breakdowns had origins in the financial sector.

For example, the Knickerbocker Crisis started from an attempt to corner the market on the United Copper Company.

When that failed, it led to the collapse of the Knickerbocker Trust Company. It was the third-largest trust in New York City at the time.

That collapse spread across the country as people rushed to withdraw their money from their local bank.

If not for J.P. Morgan – the financier – coming to the rescue, the whole banking system may have collapsed.

(This event is also one of the main reasons why we now have the Federal Reserve System.)

Another example is one many of you probably remember: The Great Financial Crisis of 2008. The collapse of investment bank Lehman Brothers was a trigger. But it all started long before that.

There was too much leverage all around the financial system. In real estate. In stocks. We all know what happened next.

The S&P 500 fell 57% from its highs. As much as $19.2 trillion in household wealth was wiped out. And the global economy lost more than $2 trillion in growth between 2008 and 2009.

All of it thanks to too much money and too many bad decisions… only possible thanks to our modern banking system. It allowed people to borrow large sums for next to nothing. Then leverage that borrowed money to the limit.

Money for nothing and the tips for free.

And if history is a guide, it will certainly happen again. The good news is that we can find ways to tilt the system in our favor.

All Is Not Lost

By far one of my favorite ways to combat the banking system and inflation is by owning physical gold and silver.

There’s nothing like holding a bar of gold in your hand. Even better, just knowing that I have that gold makes it easy to sleep at night.

And today, bitcoin is another tool at our disposal. True, it’s far more volatile than gold. But over time, that volatility should lessen.

Holding some bitcoin outside the banking system in your own digital “wallet” will probably go a long way.

Charles is of the same opinion, which is why he has recommended several investments that encompass these assets to his Freeport Investor subscribers.

But you also want to diversify beyond that. Stocks, bonds, vintage baseball cards… you want something that has optionality.

In other words, you want something that doesn’t just increase in value to keep up with the growing debt pile, money supply, and inflation.

It doesn’t have to be hard. You just need to know where to look. And Charles can help you with that. He starts with this video.

Regards,

John Pangere

Senior Analyst, Rogue Strategic Trader