Chief Investment Strategist, The Freeport Society

Hello, Fellow Navigator.

2024 has proven to be a whirlwind year for the market, marked by the S&P 500 boasting its strongest first-quarter performance since 2019.

But there’s another record that has largely gone unnoticed…

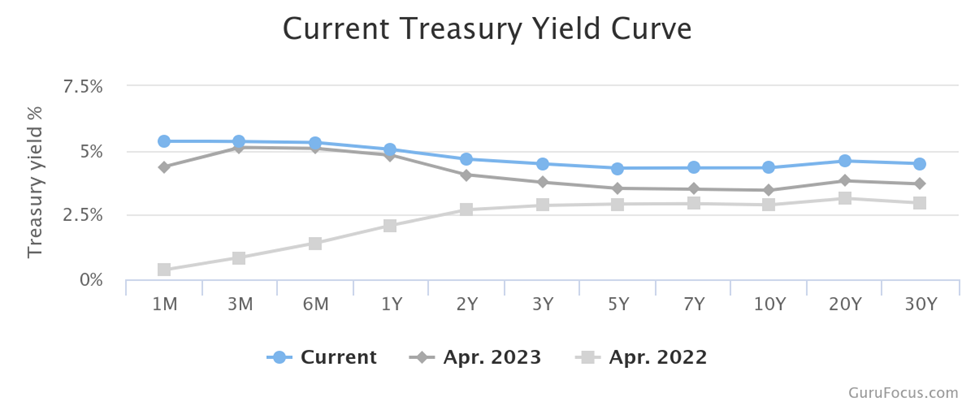

The 2-year and 10-year Treasury yield curve has been inverted for over 630 days now, dating back to its flip in early July 2022. That surpasses the disco-era 624-day inversion witnessed back in 1978.

For the uninitiated, an inverted yield curve occurs when short-term yields are higher than long-term yields. Presently, the 2-year Treasury yield sits at 4.7%, compared to 4.3% for the 10-year note. Historically, this inversion been one of the most reliable signs of a pending recession… and the sort of thing that gives Wall Street indigestion.

So, who’s to blame for this inversion… and what can be done about it? Unsurprisingly, look no further than the Federal Reserve.

Due in large part to the Fed’s money-printing experiments during the pandemic, consumer price inflation soared to 40-year highs in 2022, peaking at a staggering 9.1% that June. To tame this inflationary beast they let loose, the Fed aggressively hiked its key interest rate.

At the June 2022 Federal Open Market Committee (FOMC) meeting, Chairman Jerome Powell jacked up the Fed funds rate by a massive 75 basis points to a targeted range of 1.5% to 1.75%. And to show that they meant business, they repeated the feat in July, hiking rates by another 75 basis points to 2.25% to 2.5%.

Between March 2022 and July 2023, the Fed went on the most aggressive rate-hike campaign in its 110-year history, tallying up a total of 11 increases. This pushed short-term yields over long-term yields, where they have remained parked for nearly two full years.

Now, let’s take a look at why this inversion matters… and what the Fed might do to fix this mess they created.

Why Your Bank Is Screwed

Remember that bond prices and bond yields move in opposite directions. When bond yields are rising, bond prices are falling, and vice versa. This is because the price of existing bonds must adjust to be competitive with newer bonds issued at higher yields. If a new bond is issued with a yield of 5%, those old 4% bonds you owned must fall in value to the point that their yield rises to the new market rate of 5%.

Longer-term securities typically command higher interest rates. Investors demand juicier yields in exchange for accepting more risk and having their cash tied up for longer.

So, a normal, healthy yield curve is upward sloping, as you can see in the April 2022 line in the chart below.

But since 2023, short-term yields have been higher than long-term yields. This inverted yield curve, where 2-year bonds yield more than 10-year bonds, has accurately foreshadowed every recession over the past half-century.

The last prolonged inversion of the Treasury yield curve occurred in 2006-2007, preceding the 2008 recession.

Banks borrow short term and lend long term, taking advantage of the normal spread between short-term and long-term rates. So as long as the yield curve remains inverted, their business model is at risk. And any hiccup in the banking system reverberates across all sectors.

Why this matters: An inverted Treasury yield curve has a massive impact on the markets and the broader economy… and the longer it stays inverted, the more likely it is that something “breaks.”

That’s why Mr. Market is watching the Fed’s next moves like a hawk…

What Happened This Past Week?

The culprit behind the surge in the 10-year Treasury yield this past week was the March ISM manufacturing report. The Manufacturing Purchasing Managers Index clocked in at 50.3% in March after contracting for 16 consecutive months. Both the New Orders Index and Production have also bounced back above 50%.

Additionally, nine out of the 15 manufacturing industries reported expansion in March. Readings over 50 mean there is growth, whereas readings under 50 mean that production is falling.

While the sudden pop in growth after months of slowing might sound like good news, it means that the Fed is likely to cut rates a lot more slowly… if it cuts rates at all.

A lot is riding on when the Fed starts cutting… and by how much. A lot of the bullish sentiment in the stock market is based on a belief that the Fed will be dumping liquidity back into the market via lower rates. But what if that doesn’t happen?

Powell insists that the Fed is still on track to cut rates later this year. But I believe we may have a major surprise coming… and my friend Louis Navellier is hosting an Election Shock Summit next Wednesday, April 10, at 8 p.m. Eastern time to hash this out.

Louis, along with a special guest, will share their expectations on the Fed cut rates… and why May 1is a critical date.

This shock could not just throw financial markets into chaos…

But directly impact the presidential election results this year.

Reserve your spot by clicking here.

To life, liberty, and the pursuit of wealth.