Chief Investment Strategist, The Freeport Society

I wanted to buy a house this year.

It just made investment sense because real estate is a natural inflation hedge. Property has been a preferred asset class of the wealthy since the dawn of civilization.

I had the house picked out… but didn’t end up buying. When mortgage rates are at 20-year highs, property taxes are soaring thanks to bubbly home prices, and inflation across the board has made the cost of living and basic upkeep vastly more expensive… the numbers simply don’t work.

For much of this year, mortgage rates have climbed steadily, touching 8% in October. That made the typical principal and interest payments about double the levels of two years ago. And payments weren’t exactly cheap even then because the price of the average home rose by half between 2020 and 2022.

The result is that the real estate market has been in a deep freeze. People can’t afford expensive houses and even more expensive mortgages. Those who own their home, can’t afford to get a new mortgage. So, the only people buying were those with no choice. All of this kept property prices high.

News out this week indicates that the declining interest rates might be thawing the market a bit. I’m skeptical. So is our Freeport Society friend, Michael A. Gayed of The Lead-Lag Report. He recently penned a thought-provoking piece exploring the housing market bust that most people seem oblivious to. With his kind permission, we’re sharing this with you today. Visit www.leadlagreport.com for more from Michael.

Over to you, Michael…

The Housing Market Bust?

It’s Already Underway

As we head towards the home stretch of 2023, I maintain my belief that two events are more likely than not to occur that will drag the economy into recession – a major credit event and/or the housing market going bust.

We’ve got data suggesting that we’re already making progress on both fronts, but it’s the latter that presented some particularly strong evidence over the past few weeks.

A lot of people will point to the Case-Shiller home price index as evidence that the housing market is still fine (the national home price index just hit a record high in September).

While that may be true for now, there are a few caveats to this.

First, the index is a lagging indicator and could take time to catch up to current conditions, and second, it doesn’t reflect what’s going on in the commercial real estate space, which could ultimately be in much worse shape.

Plus, do people really think that mortgage rates can go from 3% to nearly 8% in just two years’ time without a negative impact on the housing market?

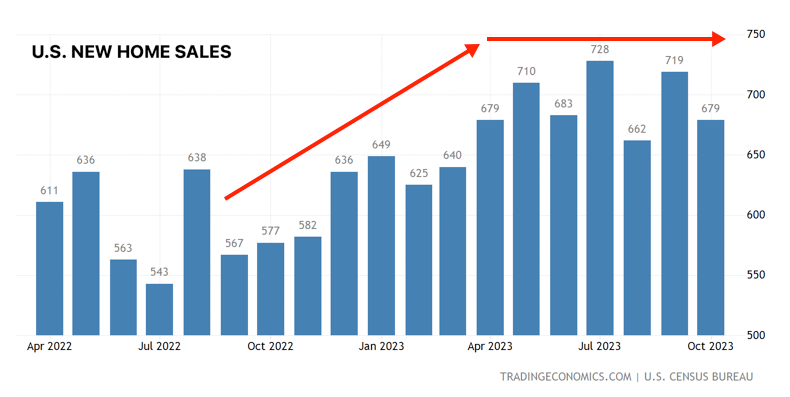

The big shoe to drop just earlier this week was new home sales in the United States. Not only did the October number miss expectations by a wide margin, but sales are now running at about the same rate as they were back in April.

This is important because it’s new homes and new construction that have driven the post-COVID boom in housing. New home sales continued to rise for a while even in the face of higher mortgage rates, but it looks like the momentum has finally stalled out.

With some volatility along the way, sales have been flat for the past seven months. This shouldn’t be terribly surprising at all, although, for some reason, it seems to be sliding under the radar.

With home prices still at extraordinary levels relative to their historical trends and higher interest rates significantly adding to the expense of financing those new homes, it was just a matter of time before homebuyers had finally had enough.

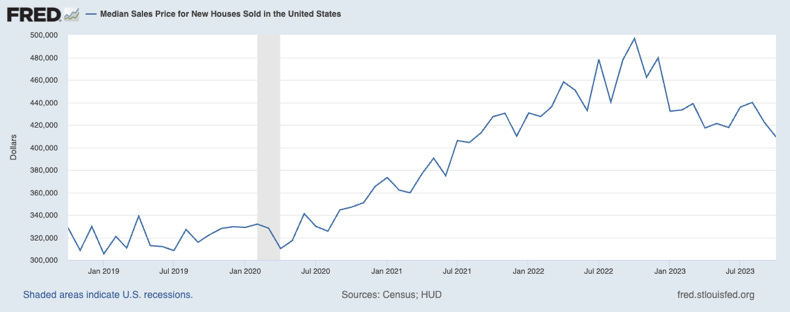

Here’s one of the biggest areas of concern for me. Perhaps the reason that new home sales are “only” flatlining instead of falling is because the cost of those new homes has already started coming way down.

Comparing new home prices from their peak in October 2022 to a year later in October 2023, there’s already been a decline of more than 17%. Only twice in the past 60 years have new home sales prices been this far below their peak – October 1970 and October 2010.

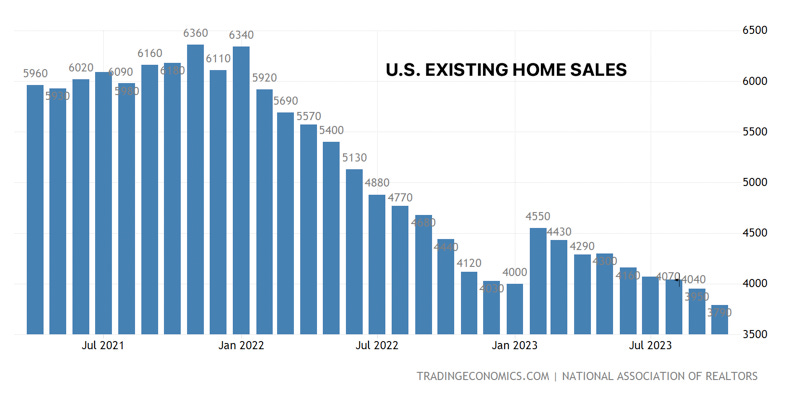

Not surprisingly, both of those occurred during recessions. If this is a sign of the early stages of a housing market breakdown, there’s not much of a safety net in place that could mitigate the impact. The existing home sales market has been in a state of steady decline for the past two years.

The October 2023 print of a 3.79-million-unit annualized rate is the lowest since the middle of 2010.

Tell me about how this is a strong housing market again?

We know that there are a couple of factors in play that are probably preventing the housing market decline from being worse. The vast majority of homeowners locked in mortgage rates when they were at record lows over the past few years.

You can argue that people being “held prisoner” in their homes because it’s far too expensive to take on a new house with a new mortgage is a bad thing, but it also means that people aren’t necessarily looking to get out of their houses or their mortgages in the way they were during the financial crisis.

Back then, owners were looking for any way to stop the bleeding on their overleveraged position and declining home price. Today, they’re locked in and can simply stay in place.

Additionally, a lot of potential homebuyers have already left the market. The extra demand that saw almost every house on the market go for above asking price has largely mitigated (although it’s still happening in some places).

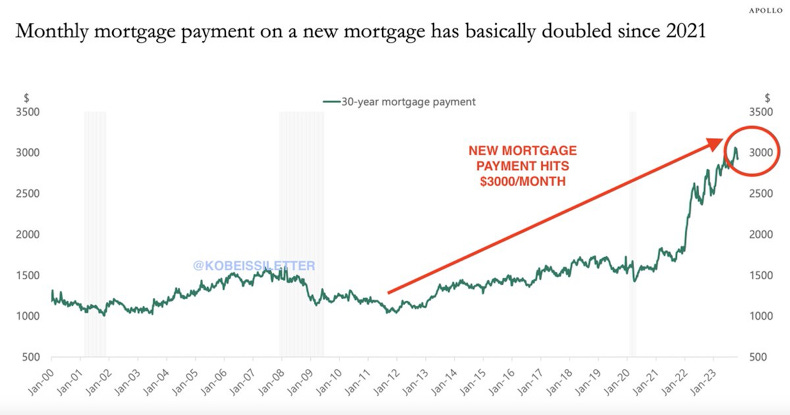

If a big source of demand is gone, you’ve suddenly got the catalyst for a normalization in the supply/demand curve that brings prices further back down to earth. But here’s the one chart that I can’t help getting out of my head.

The average monthly payment on new mortgages has doubled in the last three years!

Granted, payments have not doubled for everybody, but it’s happening to enough people that the combination of this and high inflation has likely pushed a lot of people to the financial brink.

Whether you want to look at savings balances, credit card debt levels, the use of “buy now, pay later” plans or something else, there’s a strong sense that the consumer has nearly run out of gas.

If the demand for housing is already in decline, it could be much worse 6 months from now.

Right now, most investors are banking on another Santa Claus rally and a solid December to close out the year. It may happen or it may not, but the broader economic signals currently are not supporting it.

Michael A. Gayed is the Publisher of The Lead-Lag Report, and Portfolio Manager at Tidal Financial Group, an investment management company specializing in ETF-focused research, investment strategies, and services designed for financial advisors, RIAs, family offices, and investment managers.