Chief Investment Strategist, The Freeport Society

I know better than to say “never.” The list of things that I said I would never do and yet ended up doing is long. But I can tell you with absolute certainty that you will never see me in a retail store on Black Friday.

Not in this life. Not in hell. Never.

No matter how badly I might want to buy something, the joy I would experience from owning it just isn’t worth the degradation to my soul from fighting mall traffic with the estimated 130 million other Americans pushing to get in the door. I’d rather pay full retail price or, better, not buy it at all.

Interestingly enough, I read that 12% of Black Friday shoppers are drunk, and that actually makes sense. That’s the only way I could imagine it being (almost) tolerable.

I spent Black Friday fishing for piranha in the Peruvian Amazon jungle with my sons. Grilled piranha may be a poor substitute for Thanksgiving turkey, but it beats fighting mall crowds. To add to Bill Bonner’s discussion of “fake capital” from yesterday, let’s take a look at the early numbers.

Magic Money

Data from Mastercard showed overall Black Friday sales up 2.5% from last year. In-store sales (as opposed to online) were up 1.1%.

But remember, those numbers aren’t adjusted for inflation, and CPI inflation has been running at an average of over 4% for the past year. So, spending is actually down over last year in real terms, and not by a small amount.

It looks even more fake when you dig into how it was all paid for. Data from Adobe Analytics showed that buy now, pay later (BNPL) services accounted for $760 million in Black Friday weekend shopping, up 20% from last year.

Why might BNPL be surging in popularity?

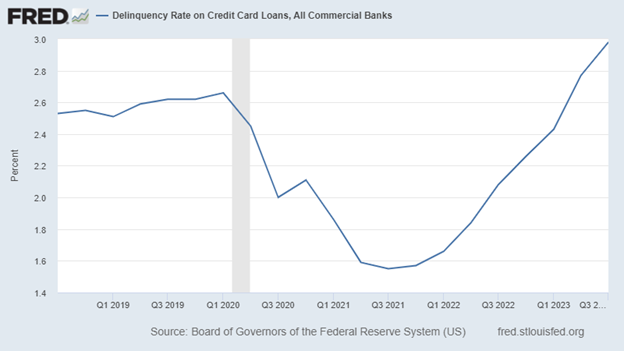

That’s a good question. My educated guess is that it has something to do with credit cards already being maxed out. Credit card balances topped $1 trillion for the first time this year, and delinquency rates are now at five-year highs. And the effect of student loan payments restarting isn’t even showing up in the data yet.

This credit card delinquency rate chart crystalizes the picture here…

So, those Black Friday figures… while not exactly strong to begin with… are only made possible with new and creative ways to borrow. This year promises to be the most heavily indebted Christmas in history.

Let me be clear here. This isn’t information being splashed all over the headlines. The “impartial” media is mostly gasping at the huge Black Friday sales without any care in the world for reporting the true depth of the problem… or even the problem itself. Here at The Freeport Society, we call B.S. on that nonsense.

A Good Tool in the Wrong Hands

Debt is not inherently good or evil. It’s a tool, nothing less and nothing more.

When used wisely and in moderation – such as to buy an income-producing asset or expand a healthy business – debt can be an instrument of real, sustainable growth.

But when debt is used for current consumption, you’re not building anything. You’re using “future money” to buy something now.

And that’s America’s debt problem.

You might – might – be able to justify our government’s $1.7 trillion budget deficit if the cash being borrowed were being invested in infrastructure that could potentially fuel the growth of tomorrow.

Building out the Interstate Highway System, railroads, canals, and electrical and internet networks wasn’t cheap, and all of these projects got government funding in some form.

But the numbers don’t add up.

The Panama Canal is one of mankind’s greatest engineering accomplishments. It cost an estimated $375 million to build, which would be a little north of $12 billion in today’s dollars.

Our budget deficit today – not our national budget, but rather money we don’t have yet – could fund the construction of 142 Panama Canals… per year.

Let that sink in.

Except we’re not building 142 Panama Canals with our future dollars. We’re not building anything, actually.

What we ARE doing is borrowing to spend on regular day-to-day expenses… the government equivalent of the weekly grocery bill.

Fake Capital Revisited

Our friend Bill Bonner’s thoughts on this are exactly right. As he wrote here yesterday:

What we take from this is that something went seriously wrong with American capitalism; its best stocks and bonds have been disappointments. Speculators put billions of dollars into cryptos, NFTs, and zombie stock – leading to huge losses. Prudent investors, meanwhile, tried to protect their wealth with U.S. Treasury bonds which pretended to be ‘safe;’ they lost a third of their money over the last 38 months.

Multiply those miscalculations and nonsense speculations by millions…all up and down the capital structure…and you get one weird, fakey economy – in which real values were falsified by fake money, lent out at fake interest rates, to fund fake investments by fake entrepreneurs in fake industries that produced fake gains.

About that…

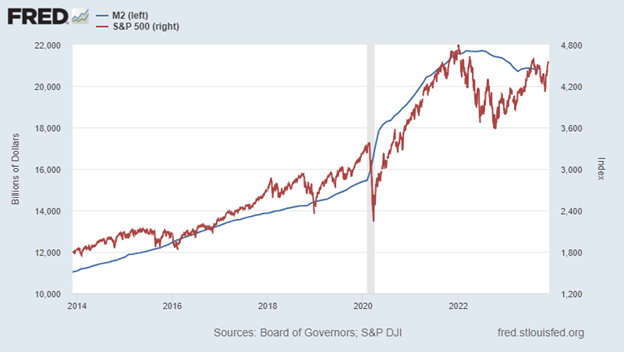

Graphing the growth of the money supply (M2, the blue line on the next chart) alongside the S&P 500 (the red line) paints us a vivid picture of just how fake the market gains of the past few years have been.

As the Federal Reserve boosted the money supply through easy monetary policy, it also goosed the stock market. And as soon as the money supply stopped growing last year, Wall Street’s fun stopped, too.

I don’t want fake capital. I don’t want government IOUs that are guaranteed to be repaid in devalued dollars… if they’re paid at all.

I don’t want garbage companies like WeWork, pawned off on desperate investors by snake-oil salesmen with access to cheap private equity money.

I want the real thing.

I want real investments in real businesses earning real, non-debt-fueled profits. And I identify five of them for you in my special report Five Unapologetically Profitable Stocks. Check it out here.