Chief Investment Strategist, The Freeport Society

In a move that surprised no-one, the Federal Reserve cut its benchmark interest rate by 0.25% yesterday. They decided that the risks to the job market were greater than the risk of rising inflation.

They’re wrong.

Historians will view this as a major unforced error because inflation really is trending higher again.

But, for the moment, lower rates are the reality.

This was arguably the most anticipated rate decision in history given the political intrigue surrounding it. President Donald Trump has been loudly pressuring the central bank to cut rates, going as far as to threaten to fire Chair Jerome Powell and actually firing Governor Lisa Cook (though the courts have put that firing on hold for now.)

So, now what?

Let’s talk about what that means for our stock portfolios… and everything else.

What Did the Fed Actually Say?

The Fed funds rate is now 4% to 4.25%.

But Mr. Market wants to know what the central bank has cooking for the rest of this year and beyond.

That’s where it gets interesting…

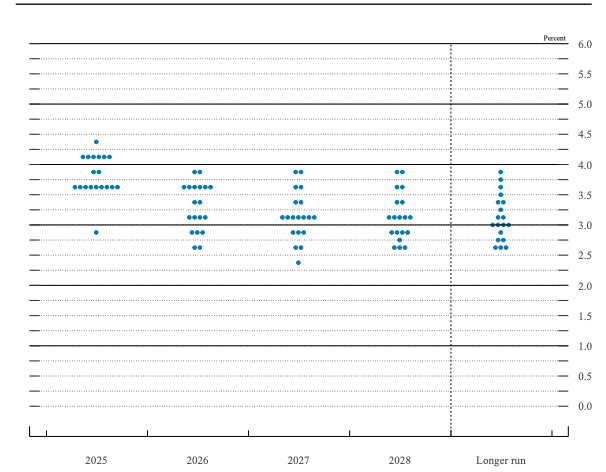

Each policy meeting, the members of the Fed Open Market Committee (FOMC) – the body that sets rates – does an internal poll of where each member thinks interest rates should be. This is the infamous “dot plot” you hear mentioned in the financial press.

FOMC Dot Plot for “Appropriate” Fed Funds Rate

Looks like incomprehensible hieroglyphics. I’ll decode them for you.

This year, one member of the committee believes rates should be pegged at 4.25% – 4.50%. That’s where we were before yesterday’s cut.

Another six members believe rates should stay parked at 4% to 4.25%.

The lion’s share of the committee – nine in total – wanted to see rates at 3.5% to 3.75% before year end, suggesting two more rate cuts from here.

One wild cowboy expected the Fed to slash rates another 1.25% all the way down to 2.75% to 3%.

They don’t tell us who voted for which dot… but my money’s on the newest addition Stephen Miran as that cowboy.

Miran is the architect of the “Mar-a-Lago Accord,” which proposed lowering the value of the dollar to boost exports. He’s well known as an uber dove.

Now, the dot plot isn’t chiseled in stone. It’s a snapshot of the Fed’s decisionmakers’ thinking at a single point in time and can turn on a dime. But for the time being, the Fed is telling us that they expect rates to be about half a percent lower by the end of the year and roughly another half percent lower by the end of next year.

What’s the Real Rate?

Remember, the rates the Fed sets are nominal rates. That means they aren’t adjusted for inflation… inflation that happens to still be clocking in at around 3% per year.

That means that the real, inflation-adjusted rate will be a measly 0.5% to 0.75% by year end.

You’re not exactly getting rich on that.

Meanwhile, the Fed’s expectations for GDP growth aren’t inspiring either.

The average estimate among the Fed’s committee members was that the economy would grow at less than 2% per year through at least 2028. They don’t expect inflation to return to their 2% target until 2028.

In other words, the Fed expects stagflation: sluggish growth combined with sticky inflation.

Great.

What do we do about it?

Not a whole lot, unfortunately.

The Fed has aggressively suppressed interest rates for most of the past 25 years. That’s not going to change any time soon. All else equal, that means persistent inflation, flat bond yields. and a weaker dollar.

The only thing you can really do is protect yourself with inflation hedges. Gold should be part of that story. High-quality stocks too, though it does look more and more like stocks are in a bubble. This probably isn’t the best time to add major long-term stock exposure.

Perhaps the best advice is simply to stay nimble and get more comfortable with shorter-term trading. You can buy expensive, bubbly stocks so long as you have rules in place to sell them if the trade goes the wrong way on you.

Or…

You could not buy bubbly stocks and instead by ones that are lesser known and potentially more explosive. This is one of InvestorPlace Senior Analyst Eric Fry’s approach. With more than three decades of experience and the uncanny knack to uncover 10 baggers, his “buy this not that” signal has proved its value over and over.

He shows you how it works, and what it’s saying to buy and not buy, in this free presentation.

To life, liberty, and the pursuit of wealth.