Chief Investment Strategist, The Freeport Society

Central bank independence is critically important to maintaining confidence in the U.S. dollar.

Yet the Fed’s abysmal performance over the past 25 years shows that it also needs major reforms to maintain that confidence, and reforming the Fed by definition means taking away some of that independence… which erodes confidence.

It’s a Catch 22.

So, today, let’s talk about that op-ed that Treasury Secretary Scott Bessent wrote for the Wall Street Journal last week.

Per Bessent,

The Fed’s new operating model is effectively a gain-of-function monetary policy experiment. Overuse of nonstandard policies, mission creep, and institutional bloat threaten the central bank’s independence.

We should just assume that all politicians with high and mighty words have ulterior motives… or that they’re flat-out lying to us.

We know what Bessent wants here.

He and President Donald Trump want the Fed to aggressively cut rates.

But that doesn’t mean he’s wrong, and I’ve made many of the same arguments myself about the Fed’s expanded role.

Yes, the Fed has overused nonstandard policies like quantitative easing.

Mission creep has massively expanded its mandate far beyond what Congress originally imagined for the bank.

And institutional bloat effectively locks the mission creep in place, leaving the economy and stock market dangerously dependent on the Fed’s actions.

What about some of Bessent’s other observations…

Successive interventions during and after the financial crisis of 2008 created what amounted to a de facto backstop for asset owners. This harmful cycle concentrated national wealth among those who already owned assets.

Within the corporate sector, large firms thrived by locking in cheap debt, while smaller firms reliant on floating-rate loans were squeezed as rates rose.

Homeowners saw their property values soar, largely insulated by fixed-rate mortgages. Meanwhile, younger and less affluent households, shut out of ownership and hit hardest by inflation, missed out on appreciation.

Yes, yes, and yes.

While 2008 was the start, it massively accelerated during the pandemic.

Home prices are about 50% higher than they were at the beginning of 2020. Stock prices are 120% higher.

Meanwhile, real GDP is about 12% higher.

The Fed added $5 trillion to its balance sheet, creating a lot more dollars to chase a limited number of real assets. The result was a bubble in virtually everything… one that’s still inflating today.

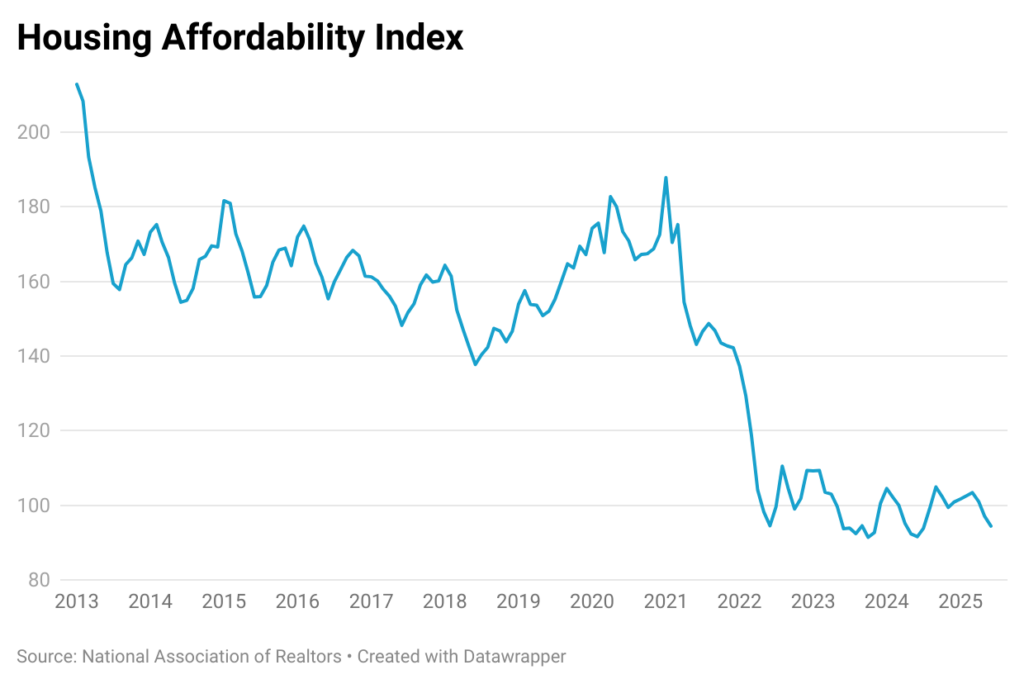

Unaffordable

Forty years ago, the median house cost 3.6 times the median income. Today, the number is 5.3 times.

This trend is clear to see in the National Association of Realtors’ Housing Affordability Index.

Anything above 100 suggests that the average family can afford the average house. Well, the index plunged in 2020 and 2021, during the Fed’s stimulus orgy, and has been trending lower ever since.

Oh, and Bessent is just getting started. There’s more…

…the Fed has blurred the lines between monetary and fiscal policy…

Entanglement with Treasury debt management creates the perception that monetary policy is being used to accommodate fiscal needs.

Expanded powers have fostered a culture in Washington that relies on the Fed to bail out the government after poor fiscal choices.

Instead of accountability, presidents and Congress have expected intervention when their policies falter. This “only game in town” dynamic has created perverse incentives for irresponsibility.

Perverse incentives for irresponsibility.

Gee, ya think?

The Fed doesn’t directly finance the government. It acts indirectly, buying bonds on the open market. But that is really a distinction without a difference. The Fed is still the buyer.

The Fed’s willingness to Hoover up government bonds gave Congress every possible incentive to spend well beyond its means.

If the Treasury had to truly go to the public hat-in-hand to ask for money, do you think interest rates would be anything close to what they are today?

Of course not. They’d be nose-bleed high.

Would you want to lend money to someone $37 trillion in debt who adds an extra $2 trillion to that total every year?

Yeah, me neither.

So, what’s the solution?

Bessent recommends limiting quantitative easing (i.e. mass bond buying) to true emergencies.

That’s a start. I recommended as much back in August.

But it doesn’t go nearly far enough.

So long as the Fed is allowed to set interest rates, it’s going to have the temptation to tinker… and inflate asset bubbles.

Interest rates – the price of money – should be set by the market, just like the prices of houses, cars, or tomatoes.

That isn’t going to happen any time soon.

No government agency ever willingly gives up power. Besides, Washington is too dependent on cheap interest rates to ever leave that responsibility to the free market.

So, what do you do about it?

You hold on to your gold and Bitcoin and any other dollar hedge you can get your hands on.

To life, liberty, and the pursuit of wealth.