Chief Investment Strategist, The Freeport Society

I don’t think I’m insane.

But when I read this little bit from Reuters yesterday… and dozens of hot takes just like it… I do start to wonder if I’ve lost my mind:

The likelihood of a Federal Reserve rate cut in September is now seen near 100% after new data showed U.S. inflation increased at a moderate pace in July.

Huh?

Core consumer price inflation (CPI) came in at 3% in July. That’s a six-month high. It’s also 50% higher than the Fed’s target of 2%. And producer price inflation (PPI) just hit its highest levels in three years based on this morning’s report.

If anything, it looks like “transitory” inflation is accelerating again rather than falling.

On what planet is that moderate?

And yet traders are indeed pricing in a 100% chance that the Fed cuts rates next month.

As of this morning, the futures markets are pricing in a 93.8% chance that Powell cuts by 0.25% and a 6.2% chance he lops it by a full 0.5%.

We’ll set aside for a moment the question of why the Fed is in the rate setting business to begin with.

Every Fed chair of the past 40 years has made a mess of the job. You’d think by now it would be obvious that the market should set rates… and not an incompetent political appointee with a built-in inflation bias.

But we’ll leave that rant for another day.

Today, let’s assume that the Fed indeed starts cutting rates in September. It’s almost universally accepted that this is “good for the stock market.”

But is it?

It intuitively makes sense.

Lower rates (at least in theory) spur economic activity by making it cheaper to take risk. They also encourage spending over saving.

Lower rates make bonds or money markets comparatively less attractive and incentivize investors to try their luck in the stock market.

And remember, stocks are priced today based on investors’ estimates of future profits. Lower interest rates make those future earnings worth more in today’s dollars, justifying higher price/earnings ratios.

But what does history tell us about past rate-cut cycles?

Let’s have a look and discuss how to position your wealth building efforts accordingly.

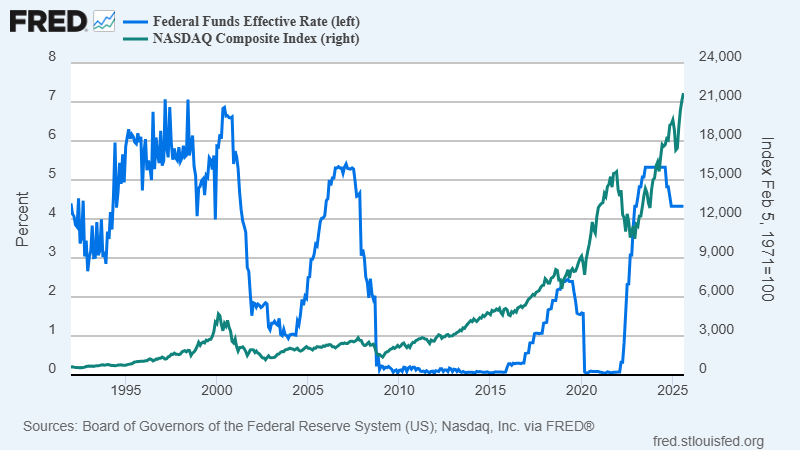

It’s No Longer Just the Fed’s Story

The following chart graphs the Nasdaq Composite (green line) alongside the effective Fed funds rate (blue line).

Study it for a second.

Really give it a good look.

Yes… falling interest rates correspond to rising stock prices… sometimes. Other times, not so much…

Most recently, at the end of last year, Powell chopped interest rates by a cumulative 1% between September and December. The market blasted higher (and continues on that trajectory nearly a year later).

But let’s remember that the market had already been trending higher for months and the Fed was only part of the equation.

The market also responded to President Donald Trump’s election and the hope of tax cuts and deregulation.

We’re also in the middle innings of the AI revolution, which is minting money for the largest tech stocks that dominate the market today. (This briefing reveals the next step in this AI revolution so don’t miss it.) It’s hard to argue any of this is a “Fed story.”

In 2020, the Fed dropped rates to zero and went the extra step of buying $5 trillion in bonds. This move more than doubled the size of its balance sheet.

And stocks exploded higher in the 2020-2021 FOMO (fear of missing out) rally.

That really was a Fed story, obviously.

But it’s not likely to be repeated in our lifetimes given the inflation it sparked. We’re still cleaning up the mess five years later.

In between, the Fed aggressively jacked up rates, which led to a brutal bear market in 2022.

So, between 2020 and 2025, we can say that the Fed had an outsized impact on the stock market.

Casting the net wider, the correlation gets murky at best.

Don’t Fight the Trend… But Be Prepared

In the late 1990s, the Fed steadily raised interest rates, and yet stocks continued to blast higher in what would eventually become the biggest stock bubble in 70 years.

When it all fell apart in 2000, the Fed started aggressively slashing rates, eventually lowering them all the way to 1%. It took three years for stocks to find a bottom and start trending higher again.

In 2005 and 2006, the Fed aggressively raised rates again… and both the stock market and the housing market boomed. In fact, the housing market boomed a little too hard, inflating into a bubble.

When the housing market collapsed at the end of 2007, ushering in the Great Financial Crisis, the Fed lowered rates to zero, something that was previously considered impossible.

Yet the market still dropped like a rock, losing more than half its value in one of the worst bear markets in history.

Investors enjoyed some really solid years between 2009 and 2015 as rates stayed anchored at zero. But the bull market continued from 2015 through the beginning of 2020, even as the Fed relentlessly pushed rates higher.

So, you tell me…

Is a quarter point rate hike next month really something to get excited about?

Or should we be more concerned that nine out of ten leading indicators point to a sluggish economy ahead?

You’re right. We should be concerned.

So what can we actually do about it?

You know me. I’m a big believer in hedging my bets.

I recommend you keep a little extra cash on hand.

I also strongly recommend you hold on to your gold and Bitcoin. All else equal, falling interest rates mean a weaker dollar, and gold and Bitcoin are two of the strongest dollar hedges available.

But I’d also advise against fighting the trend.

Stocks – and particularly the tech stocks profiting most from the AI revolution – are trending higher. We should ride that trend as long as we can.

One easy way to ride that trend higher is via the Xtrackers Artificial Intelligence and Big Data ETF (XAIX). I recommended it in the Freeport Investor in December and it’s up 44% from its April lows.

I also recommend you watch this special briefing about the next leg of the AI revolution. You’ll find the details of another stock to invest in.

To life, liberty, and the pursuit of wealth.